Today, prospective homeowners have many different questions when it comes to the timing of their home purchase. With the recent increase in interest rates, stock market volatility, and economic uncertainty, it makes sense that many buyers who would have been ready to move in 2018, are now closely scrutinizing any potential investments. While conventional wisdom encourages investing in a home as soon as a sufficient down payment is available and a mortgage pre-approval is in hand, many buyers are pausing to assess their options.

Rent Now Versus Buy Now, Refinance Later?

With limited inventory and home prices stabilizing, it’s a question that many first-time home buyers grapple with as they attempt to strategize their timing to their advantage. After all, investing in real estate is one of the most financially significant moves a person can make, and factors such as market conditions, closing fees, and financing options, can make a real difference in the total cost of the transaction. Ultimately, to make a sound decision, it’s important to consider not just the upfront cost difference between making a monthly rent payment versus a monthly mortgage payment, but beyond that – what is the true cost of waiting to buy?

Factors to consider:

-

Increased cost of renting over the period of project home ownership. On average, rent increases about 3.2% YOY nationwide, although 2021-2022 saw a significantly larger jump.

-

Total home price appreciation over the projected period of ownership.

-

Inflation over the same period (on average 3.8% YOY).

-

Mortgage interest rates – both at the time of purchase, and trends that indicate future rate movement.

The calculations can get tricky with all these factors to consider, however, it is crucial to understand how they contribute to the total cost of ownership. It is a solid case for consulting with local real estate and mortgage professionals during the home search process.

Appreciate The Risk of Waiting

Waiting on a home purchase can ultimately cost the buyer more than may initially appear. The two main factors that make the case for buying a home are:

Home appreciation – How much a property increases in value over a period of time. Amortization – The gradual payment of all interest and principal payments of a home loan.

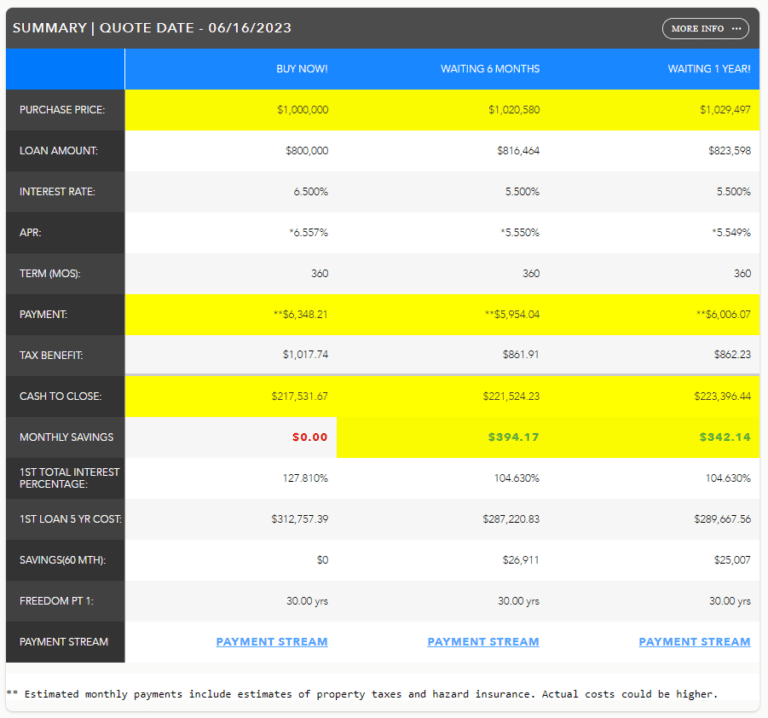

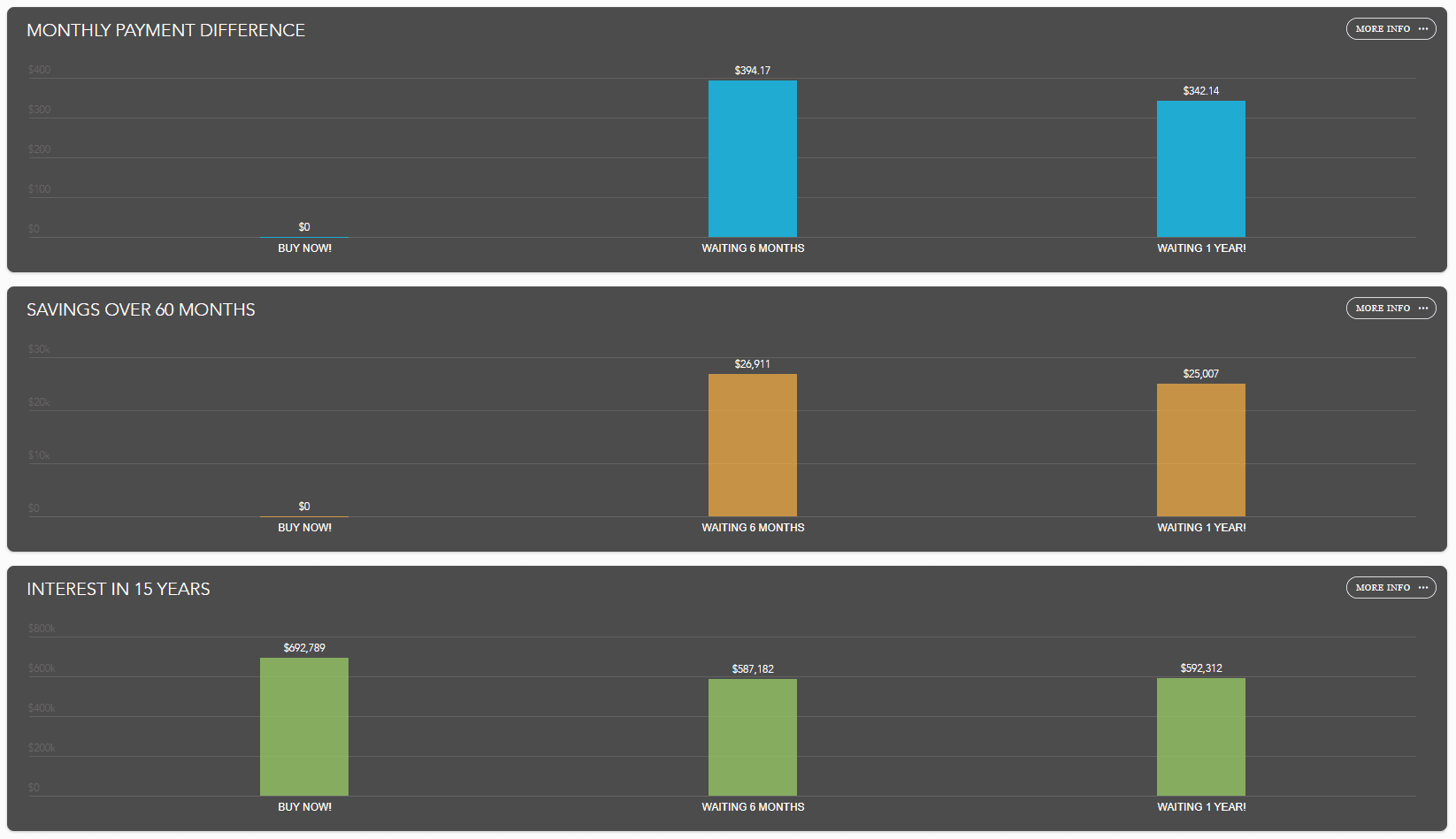

The sample quote below from our friends at OriginPoint illustrates the true cost of waiting. Note:

-

While the Buy Now option includes monthly payments of $300+.

-

The 6-month snapshot shows $20,580 in appreciation loss and $4,398 amortization, for a loss total of $24,978.

-

The 12-month snapshot shows a loss of $29,497 in property appreciation and $8,942 amortization loss, a total of $38,439.

The sooner you buy a home, with plans to refinance in a year, you will reap the benefits of both a lower rate and better monthly payment with a home that has more equity.

In real estate, it is always important to consider the financial investment from a long-term perspective, as well as upfront costs. This is especially true when deciding whether to make the jump from renting to buying your first home. Every case is unique, so consulting with local real estate and mortgage professionals during the home search process is essential to remain informed and make choices that benefit you in the future.

Explore Additional Insights and Articles

Explore Additional Insights and Articles